ITR Filing Mistakes Cost Salaried Employees Lakhs

Small errors in ITR filing can lead to huge tax bills. Avoid common mistakes to save lakhs.

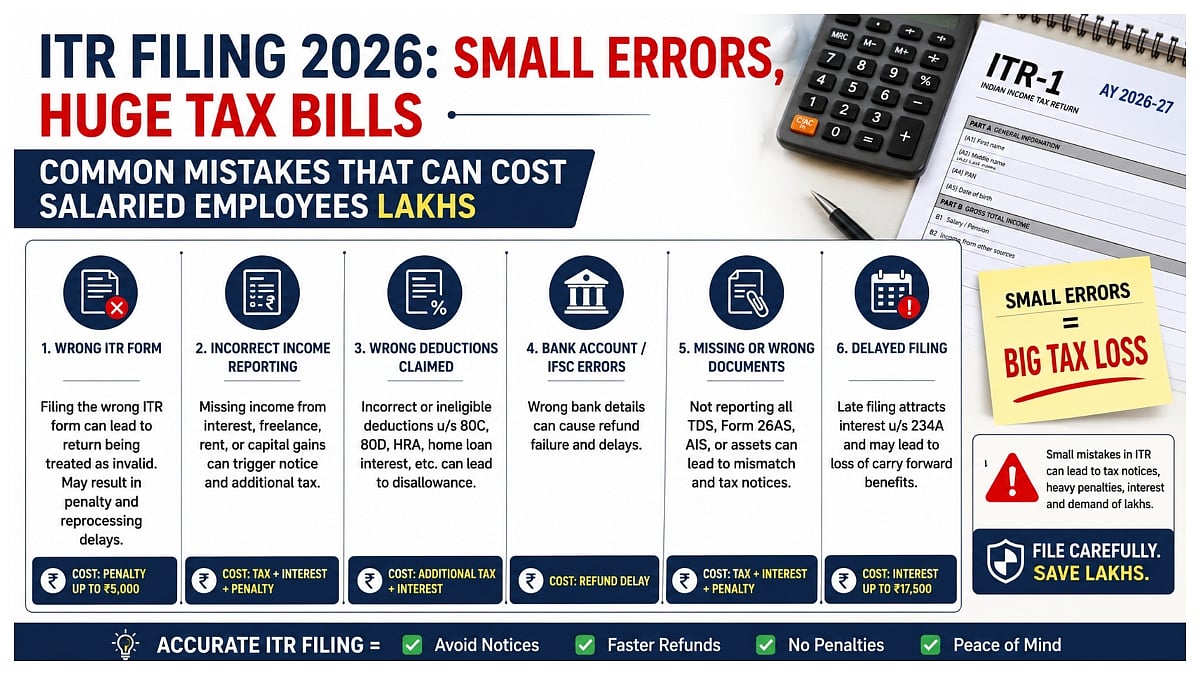

Mumbai residents are warned that filing an Income Tax Return (ITR) is no longer a simple process. With the Income Tax Department using data from various sources, even small mistakes can lead to tax notices, extra tax, interest, and penalties.

The Income Tax Department uses data from Form 26AS, the Annual Information Statement (AIS), and the Taxpayer Information Summary (TIS) to verify ITR filings. Therefore, it is crucial for salaried employees to reconcile their salary details with bank statements, investment records, capital gains statements, and other financial documents before filing their ITR.

One common mistake made by salaried taxpayers is not choosing the correct tax regime. The new tax regime offers lower tax rates but limits many exemptions and deductions, including HRA, LTA, home loan interest, and several deductions under Sections 80C and 80D. Taxpayers should calculate their tax liability under both the old and new regimes before making a choice.

Claiming deductions without valid proof is another common mistake. Taxpayers should verify their insurance premiums, ELSS investments, provident fund contributions, home loan certificates, and donation receipts before claiming deductions. Failure to do so can result in future tax demands.

Reporting all income is also crucial. Capital gains from shares, mutual funds, ESOPs, or property must be reported correctly. Errors in calculating long-term or short-term gains, acquisition cost, or exemptions can result in higher tax liability. Bonus, arrears, joining bonus, severance pay, and retirement benefits also require proper tax treatment.

Resident and ordinarily resident taxpayers must disclose foreign assets, overseas bank accounts, ESOPs, and foreign income wherever applicable. Failure to do so may attract heavy penalties under the Black Money Act. Before filing, taxpayers should ensure their bank account details are correct, linked with their PAN, and pre-validated to avoid refund delays.

Finally, e-verification of the ITR within the prescribed timeline is essential. An unverified return may be treated as invalid, delaying refunds and inviting further compliance issues. Careful reconciliation, proper documentation, and timely verification can help employees avoid costly mistakes while ensuring all eligible tax benefits are claimed.

The Income Tax Department has introduced various tools to help taxpayers file their ITR correctly. The income tax portal provides a step-by-step guide to help taxpayers choose the right ITR form and reduce filing errors.

In conclusion, salaried employees in Mumbai must be cautious when filing their ITR to avoid costly mistakes. By choosing the correct tax regime, claiming deductions correctly, reporting all income, and disclosing foreign assets, taxpayers can ensure they receive all eligible tax benefits and avoid hefty penalties.

The importance of accurate ITR filing cannot be overstated. With the Income Tax Department cracking down on tax evasion, it is crucial for taxpayers to ensure they are in compliance with all tax laws and regulations. By taking the time to carefully review their ITR filing, salaried employees in Mumbai can avoid costly mistakes and ensure a smooth tax filing process.

The new tax regime and the use of data from various sources have made ITR filing more complex. However, with the right guidance and tools, taxpayers can navigate the process with ease. It is essential for salaried employees to stay informed about the latest tax laws and regulations to ensure they are in compliance and receiving all eligible tax benefits.

In the end, careful planning and attention to detail are key to avoiding costly mistakes when filing an ITR. By taking the time to review their tax filing carefully, salaried employees in Mumbai can ensure they are in compliance with all tax laws and regulations and receiving all eligible tax benefits.