Report FD Interest Correctly To Avoid Tax Notices

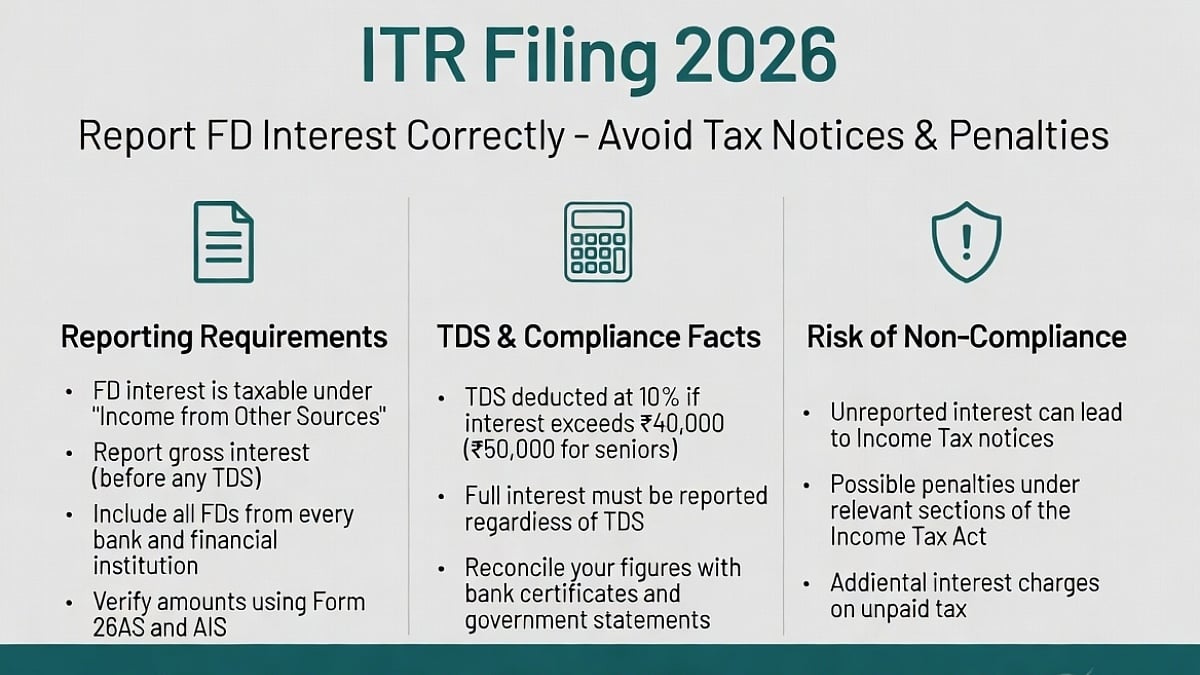

Taxpayers must disclose FD interest in ITR, even if TDS is deducted. Mismatch can lead to notices and penalties.

Mumbai taxpayers are reminded to report their fixed deposit interest correctly when filing their income tax returns. This is crucial, as leaving out this information can lead to problems, including tax notices and penalties.

The interest earned from fixed deposits must be added to the taxpayer's income and disclosed under 'Income from Other Sources' in the ITR. Taxpayers can find FD interest details in bank statements, interest certificates, Form 26AS, the Annual Information Statement (AIS), and the Taxpayer Information Statement (TIS).

It is essential to compare these records before filing to ensure accuracy. If there is a mismatch, taxpayers should verify the figures with the bank and report the correct amount. FD interest is taxed according to the taxpayer's applicable slab rate, which may vary depending on age, residential status, and whether the old or new tax regime is selected.

Senior citizen taxpayers choosing the old tax regime can claim a deduction of up to Rs 50,000 under Section 80TTB, covering interest from savings accounts, fixed deposits, and recurring deposits. However, this benefit is unavailable under the new tax regime. Additionally, investment in a five-year tax-saving FD may qualify for deduction under Section 80C, forming part of the overall Rs 1.5 lakh annual limit available under the section.

Banks generally deduct TDS at 10 percent under Section 194A when interest crosses the prescribed threshold. However, TDS is only an advance tax credit and does not remove the requirement to disclose the full interest income. The TDS reflected in Form 26AS can be adjusted against the final tax liability, which may lower tax payable or result in a refund.

Eligible taxpayers may submit Form 15G or Form 15H to request non-deduction of TDS, subject to prescribed conditions. It is crucial to ensure accuracy when reporting FD interest, as failure to disclose this information can create a mismatch with AIS or Form 26AS, leading to notices, additional tax, interest, or penalties.

Taxpayers are advised to carefully reconcile their records before filing to avoid errors and claim all eligible deductions and TDS credits correctly. By reporting FD interest correctly, taxpayers can avoid unnecessary notices and penalties, ensuring a smooth and hassle-free ITR filing process.

In conclusion, accurate reporting of FD interest is essential for Mumbai taxpayers to avoid tax notices and penalties. By understanding the rules and regulations surrounding FD interest, taxpayers can ensure compliance with tax laws and make the most of available deductions and credits. As the ITR filing process begins, taxpayers are reminded to prioritize accuracy and attention to detail to avoid any potential issues,